Your Health Decides Whether Your Home Equity Funds Freedom or Care

For Canadian homeowners over 55, your physical and mental health is one of the biggest hidden variables in your retirement plan. Why? Because declining independence triggers forced costs - home care ($2,000 - $3,000+ per month), accessibility renovations (up to $25,000+), or memory care ($5,000 - $8,000+ per month) - that quietly drain savings and home equity you spent decades building. Stay healthy, and you can access your wealth on your own terms. Let your health decline, and the same money gets spent reacting to a crisis. This guide shows you exactly how the two connect, and how to plan from a position of strength.

When Canadians map out retirement, they usually focus on the predictable numbers: pensions, savings, property taxes, and the value of the home. What often gets missed is the slow cost of losing independence. When mobility fades or memory slips, the financial pressure rarely arrives as one large bill. It shows up month after month: a personal support worker, a bathroom retrofit, or eventually a move into specialized care. For many senior Canadians, those costs are ultimately paid for with home equity. The real question is whether that equity gets used strategically or consumed by necessity.

The encouraging part: you have more influence over this than you think. The exercise you do this week and the puzzles you solve tonight are direct investments in your future financial flexibility. Below, we break down the true cost of losing independence, then show you how a strong body and a sharp mind help protect both your freedom and your equity.

The Hidden Retirement Costs That Quietly Consume Home Equity

The numbers behind aging in place rarely appear in a standard retirement budget. They should. Understanding them early is the first step to preventing them - and to protecting the equity you have built.

How Much Does Home Care in Canada Actually Cost?

Personal support workers (PSWs) handle the everyday tasks that become harder with age - bathing, dressing, meal preparation, and mobility support. In Canada, PSW rates typically run from $22 to $45 per hour. Even part-time help adds up fast. Families often spend $2,000 to $3,000 or more every month once regular care begins.

That is a recurring cost, not a one-time bill. Over a single year, modest part-time care can quietly consume $24,000 to $36,000 of your retirement savings - money that often comes straight out of home equity once cash reserves run thin.

How Expensive Is an Aging-in-Place Renovation?

Staying in the home you love often means modifying it for safety. According HomeEquity Bank (CHIP), a bathroom retrofit alone can run $10,000 to $25,000 or more. , a bathroom retrofit alone can run $10,000 to $25,000 or more. Common upgrades include:

- Walk-in or curbless showers with grab bars

- Widened doorways for walkers or wheelchairs

- Non-slip flooring throughout the home

- Stair lifts or wheelchair ramps

- Lever-style handles to replace knobs

There is some relief: Canada's Home Accessibility Tax Credit lets eligible seniors claim up to $20,000 in renovation expenses annually. But the upfront cost still lands on you - and here is the key point. The further your health declines before you act, the more extensive and expensive those renovations become. Planning ahead is cheaper than reacting.

The Compounding Cost of Cognitive Decline

Cognitive decline carries the heaviest price tag of all. Specialized dementia and memory care in Canada typically costs 20 - 30% more than standard long-term care, with private memory care often ranging from $5,000 to $8,000+ per month. In major centres like the Greater Toronto Area, monthly costs can climb even higher.

Unlike a one-time renovation, this is an ongoing expense that grows as care needs intensify. It is the single fastest way to deplete a lifetime of home equity. Protecting your brain is, in very real terms, protecting your largest asset.

Why Your Health Is a Home Equity Strategy

For many Canadians over 55, rising health-related costs do not just strain monthly cash flow - they put direct pressure on home equity, the largest asset in most retirement plans. Once care needs grow, that equity becomes the balance sheet that quietly absorbs them. This is why aging well is not only a health goal - it is a financial strategy. Homeowners who protect their independence keep more choice in how and when they use their equity, including whether tools like a reverse mortgage are accessed proactively from a position of strength, or reactively under pressure.

That is why retirement planning cannot stop at investment accounts and monthly budgets. It also has to include a plan for how and when your home equity might be used if your circumstances change.

Whether a tool like a reverse mortgage ends up working proactively, on your terms, or reactively, under the pressure of rising care costs, often comes down to one thing: your health and your timing.

The Physical Shield: Protecting Your Independence (and Your Equity)

Here is the encouraging truth: it is never too late to start. Research published in BMJ Open Sport & Exercise Medicine shows that adults who begin exercising later in life still gain meaningful benefits - what researchers call the late-starter bonus. Your body responds to movement at any age, building the strength, balance, and resilience that keep you in your own home longer.

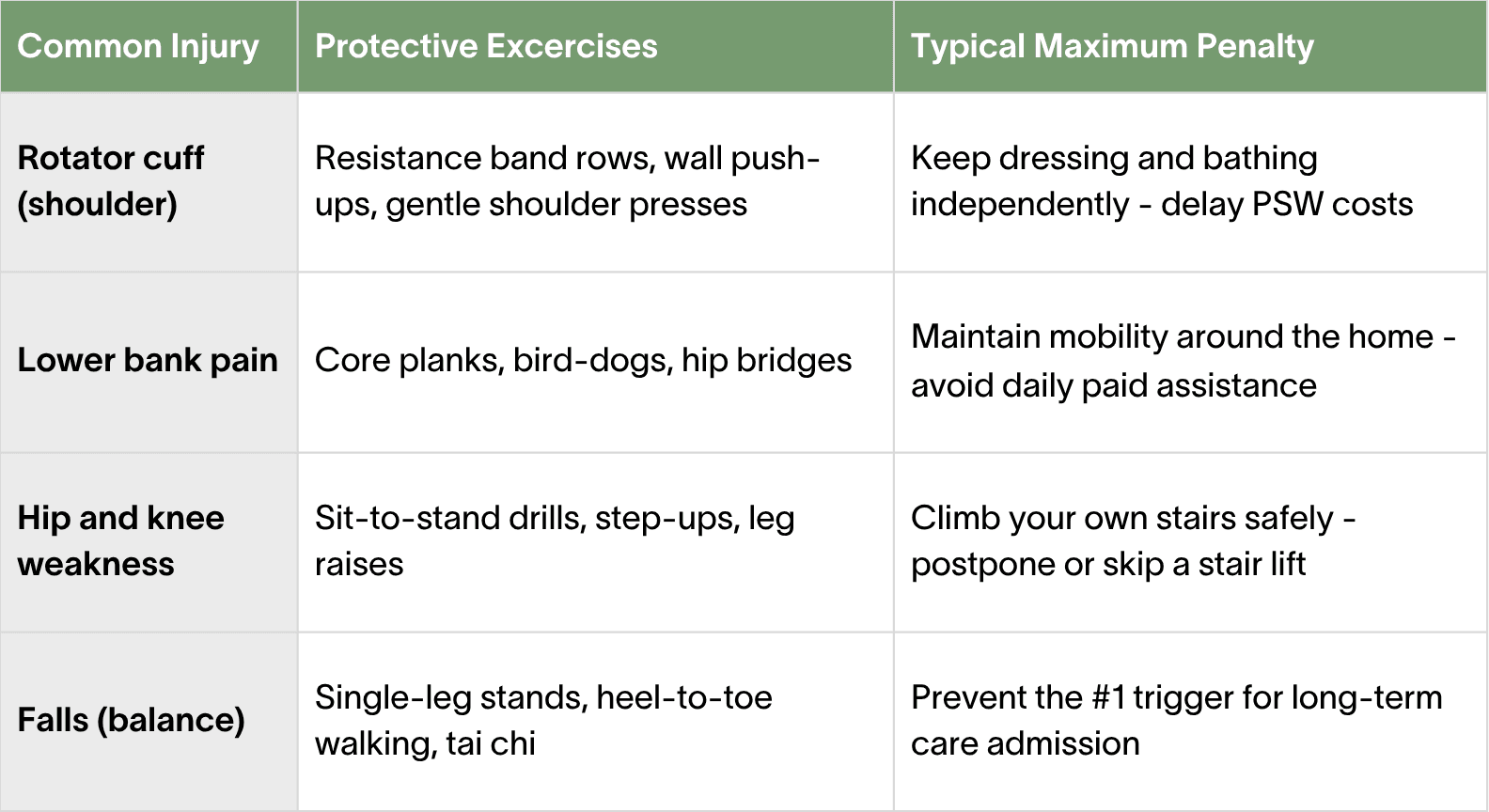

And that resilience translates directly into avoided costs. Most expensive care begins with a single preventable injury or a fall. A small investment of time now can protect tens of thousands in savings later. The goal is not to become an athlete - it is to keep doing the everyday tasks that, once lost, get outsourced at $22 to $45 an hour.

Table 1. Injury Prevention and Its Financial Payoff

Free Resources to Get Started Today

You do not need a gym membership to build this shield. These free options work right from your living room:

- Senior Fitness With Meredith - low-impact routines designed for older adults

- SilverSneakers - classes and on-demand workouts for seniors

- Leslie Sansone Walk at Home - indoor walking programs

- City programs - Toronto, Vancouver, and Calgary all offer affordable or free senior fitness classes

The Cognitive Shield: Safeguarding Your Most Expensive Risk

If physical decline outsources your tasks, cognitive decline outsources your independence entirely - and at the highest price of any care category. That makes protecting your brain the single most valuable thing you can do for your retirement budget.

The catch: not all mental activity counts. Passively watching television or scrolling a screen does little to build what scientists call cognitive reserve - the mental resilience that helps protect against decline. Reserve grows only when you challenge your brain with active, effortful tasks. Think of it as resistance training for your mind.

Mental Workouts That Build Reserve

- Social deduction and strategy games: Codenames, chess, and bridge force you to plan, deduce, and read other players. The social element adds an extra protective layer.

- Spatial and logic puzzles: Sudoku, crosswords, and similar challenges keep your reasoning sharp.

- Learning new skills: Picking up a language or a musical instrument creates fresh neural connections at any age.

The payoff is measurable. Research cited in BMJ Open found that regular board game players had a 15% lower risk of developing dementia than non-players. Put the numbers side by side: a $20 board game played weekly with friends is one of the cheapest forms of insurance against the $5,000 - $8,000+ monthly cost of memory care.

Your Health and Your Home Equity Work Together

Physical fitness and cognitive health are not separate from your financial plan - they are part of it. A strong body lowers your odds of needing PSWs and accessibility renovations. A sharp mind reduces the risk of dementia and its steep, ongoing care costs. Together, they protect the equity you have spent a lifetime building.

The two strategies reinforce each other. By investing in your body and brain today, you preserve something more valuable than the savings themselves: choice. You keep the freedom to access your home equity on your own terms tomorrow - for comfort, travel, or peace of mind - rather than being forced into it during a crisis.

So start small and start now. Twenty minutes of movement and a single game of Codenames today is a deposit into both your health and your wealth. And when you are ready to understand how your home equity fits into the bigger picture, the independent specialists at Canadian Reverse Mortgage Advistors sit on your side of the table - comparing every Canadian lender to help you plan from a position of strength, at no cost to you.

Wondering whether a reverse mortgage fits your retirement plan? Call us at (416) 821-8601 or book a call to get clear, unbiased guidance tailored to your situation.

Health, Home Equity, and Retirement FAQs

About the Author

Alexander Gasenko

Mortgage Broker, Reverse Mortgage Specialist

Alexander is the founder of Canadian Reverse Mortgage Advisors team and a licensed mortgage professional serving Ontario, British Columbia, and Alberta. With a degree in Economics and a background in banking, he’s passionate about helping Canadian seniors protect their equity and navigate rising living costs. When he’s not negotiating with lenders, Alexander shares financial insights on his YouTube channel, empowering Canadian homeowners to make informed decisions. His mission? To provide clarity and confidence for a secure financial future.