Can You Qualify for a Reverse Mortgage? Key Requirements in Canada.

A reverse mortgage is a home equity loan designed for homeowners 55 and older. It allows you to access a portion of your home equity as a tax-free advance, with no time limit or requirement to make regular monthly mortgage payments. Canadian retirees use reverse mortgages to eliminate monthly debt payments, cover lifestyle costs, fund repairs or simply enjoy more financial freedom.

Qualifying for a reverse mortgage is not based on age alone. Lenders also review your property, residency, existing debt, income, and overall eligibility before approving an application. To help you get a quick answer first, start with the approval checklist below, then read on for a more detailed explanation of each requirement.

Reverse Mortgage Requirements in Canada: Who Qualifies?

To qualify for a reverse mortgage, you generally need to meet several core requirements. Lenders will look at your age, primary residence status, property type, location, available equity, existing debt, and your ability to maintain the home.

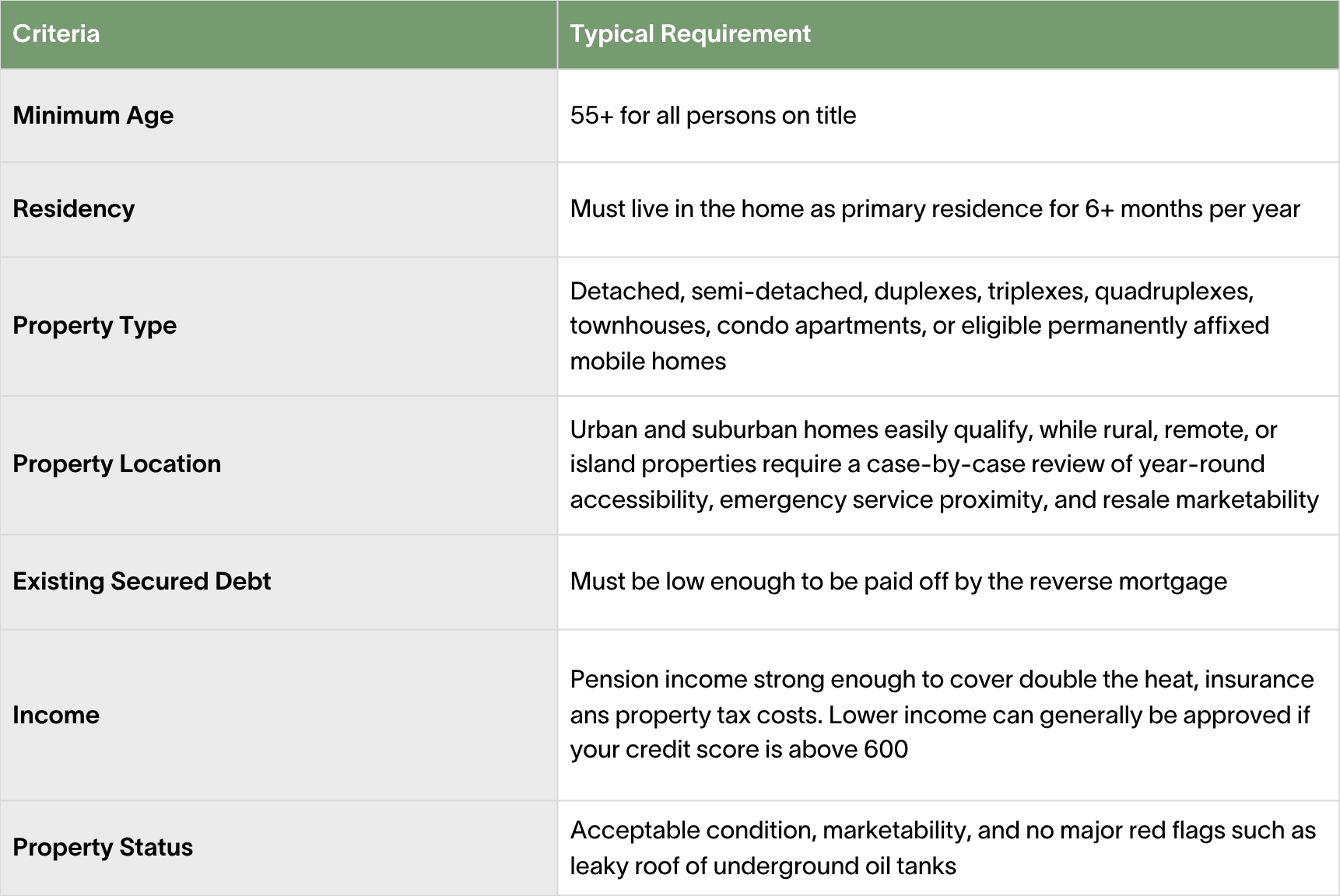

Use the quick checklist below to see the typical requirements for reverse mortgage approval in Canada. If you would like more detail on any of these criteria - the sections below explain how lenders assess each requirement.

Table 1. Reverse Mortgage Eligibility Requirements in Canada

1. Age Requirements

The most fundamental requirement for getting a reverse mortgage in Canada is age. Every person listed on the title must be 55 or older. This is a firm rule - if one owner is under 55, the application cannot proceed.

Why age matters

Your age does more than just determine eligibility - it also dictates how much equity you can access.

Reverse mortgages in Canada include a no-negative-equity guarantee, meaning you will never owe more than your home is worth. To manage this, lenders offer lower initial borrowing limits to younger borrowers, ensuring the loan remains sustainable for the bank over an expended time period.

In general:

- Younger borrowers typically qualify for a lower percentage of their home’s value.

- Borrowing power increases as you get older, often with sizable improvements at key milestones like ages 60 and 70.

2. Property Type and Location Requirements

Reverse mortgages are available for most common residential property types, provided the home is marketable, and meets lender standards.

Property types that qualify

- Single detached homes

- Semi-detached homes

- Detached duplexes, triplexes or quadruplexes

- Townhomes

- Condominium apartments

- Some permanently affixed mobile homes, depending on specific lender rules

Location matters too

Homes in major urban and suburban markets are usually easier to qualify. While rural and remote properties can get approved, lenders will review them more carefully.

They may look at:

- Year - round road access

- Ferry or bridge access, if applicable

- Distance to emergency services

- Local demand and resale potential

- Overall marketability of the property

If your home is on an island or in a remote community, the property is often reviewed on a case-by-case basis.

3. Residency Requirements

Reverse mortgages are designed to help you age in place, so residency requirements are an important part of the qualification process.

Primary residence rule

The property must be your primary residence, meaning you must live in it for at least six months of the year.

If the home is used primarily as:

- A rental property

- A seasonal investment property

- A second home you do not occupy enough

It will typically not qualify. An exception to this is the CHIP Reverse Mortgage by HomeEquity Bank. HomeEquity Bank is the only bank that allows you to bundle two or more properties under one reverse mortgage. You can combine your primary residence with up to two other properties for a total of three.

Can a property with rental income still qualify?

Sometimes, yes.

If you live in one part of the property and rent out another, the home may still be eligible. This applies to:

- Homes with legal secondary suites

- Multi-unit properties where you occupy one unit

In these cases, the lender may you look at the full property under one application, provided you still live there as your main residence.

4. Credit and Income Requirements

One of the biggest advantages of a reverse mortgage is its flexible income qualification criteria. While the mortgage stress test still applies, its purpose is different - it's used to confirm you can comfortably cover ongoing property expenses like taxes, insurance, and maintenance, not mortgage payments.

What lenders want to see

Lenders want to feel confident that you can continue paying for:

- Property taxes

- Home insurance

- Heating costs

- Basic home upkeep

How lenders verify your income

Lenders generally verify your ability to cover these ongoing costs in one of two ways:

- Income Confirmation: As a general guideline, lenders look for your total monthly income to be at least twice the amount of your property taxes, home insurance, and heating costs to ensure you have enough left over for all other living expenses.

- Credit Score Assessment: A credit score of 600 or higher can demonstrate financial reliability, even if your income is insufficient. However, depending on the income shortfall, lenders might set aside a holdback from your advance. This means you can still get a reverse mortgage, but the total amount you receive will be lower.

5. Existing Mortgage and HELOC Limits

You can apply for a reverse mortgage even if you currently have debt secured against your home, such as a traditional mortgage or a HELOC. In fact, many people use a reverse mortgage specifically to eliminate their monthly mortgage payments when their home is not fully paid off.

However, any existing secured debt must be paid off in full from the proceeds of the reverse mortgage at closing. The new reverse mortgage lender requires first-lien position, meaning they must be first in line to be repaid, which is why your existing mortgage must be cleared completely.

Therefore, the reverse mortgage you qualify for must be large enough to cover the entire balance of your existing mortgage, HELOC, or other secured loans. If the approved reverse mortgage amount is insufficient to pay off these debts, you cannot proceed unless you can cover the shortfall with other funds at closing.

Curious how much tax-free funds you could unlock? Try the Reverse Mortgage Calculator for a personalized estimate in under 30 seconds.

6. Property Condition Standards

The condition of your home can affect your reverse mortgage estimate. While minor wear and cosmetic aging are widely acceptable, lenders heavily scrutinize issues that create marketability concerns or environmental risks.

Property issues that can affect your estimate

- Structural concerns and deferred maintenance

- Non-municipal water sources

- Oil heating and oil tanks

- Large acreage

- Condominium special assessments

Not sure if you qualify, or want to discuss your unique situation? Call us at (416) 821-8601 or book a meeting to get clear, personalized guidance on your options.

Final Thoughts on Reverse Mortgage Eligibility in Canada

A reverse mortgage can be an excellent tool, but eligibility depends on more than just age. Lenders also consider your property, residency, equity, and existing debts.

The good news is that qualification is often more flexible than people expect. Even with a modest income or bruised credit, there is often a path to approval.

Canadian Reverse Mortgage Eligibility FAQs

About the Author

Alexander Gasenko

Mortgage Broker, Reverse Mortgage Specialist

Alexander is the founder of Canadian Reverse Mortgage Advisors team and a licensed mortgage professional serving Ontario, British Columbia, and Alberta. With a degree in Economics and a background in banking, he’s passionate about helping Canadian seniors protect their equity and navigate rising living costs. When he’s not negotiating with lenders, Alexander shares financial insights on his YouTube channel, empowering Canadian homeowners to make informed decisions. His mission? To provide clarity and confidence for a secure financial future.