Refinancing vs RRSP Withdrawal: How to Access $100,000 in Retirement Without Wrecking Your Wealth

When you need an extra $100,000 in retirement, you generally have two broad directions to choose from. You can borrow against the equity in your home, or you can pull the cash out of your RRSP.

Throughout this article, we use "refinancing" the way homeowners actually search for it: any strategy that unlocks the value in your home without selling it. That umbrella covers three distinct products: a conventional cash-out refinance, a secured HELOC, and a reverse mortgage.

While textbook definitions sometimes separate them, the reality is that almost all of them require a refinance in practice. If you already have a mortgage, you can rarely just "tack" a HELOC or a reverse mortgage on top; you almost always have to break, pay off, or restructure your existing loan to set them up.

Because unlocking your equity virtually always forces you to rewrite your current mortgage contract, we treat all three as refinances here. We compare all three head-to-head against a competently planned RRSP withdrawal, with an unsecured line of credit included as a standalone benchmark.

We treat our retirees as individual taxpayers, apply a consistent time-value-of-money lens to every option, and rank each path over a full 20-year horizon. By the end, you will understand exactly how each strategy truly performs when it is measured on a fair playing field.

Important Compliance Disclosure — Please Read First

Before we get into the numbers, let's be completely transparent about the methodology, limitations, and assumptions behind this model.

- This is one specific scenario. Every figure is built around a single, fixed situation: a $100,000 lump-sum net cash need, a household base income of $30,000 from CPP and OAS, and a mortgage-free home worth $400,000. Change those inputs, and the math changes too.

- Canada taxes individuals, not couples. This model assesses taxes and benefit clawbacks per person, assuming a strategic, equal split of withdrawals between spouses (or a RRIF income-splitting election where the savings sit in one name).

- A harmonized 20-year lens. Every monthly payment stream is evaluated using a 6% annual opportunity cost. In plain terms, any dollar paid out of pocket is treated as money that could have stayed invested and compounded at 6% over 20 years — the same opportunity cost applied to an RRSP withdrawal. One asterisk: because RRSP dollars are pre-tax and home equity is tax-free, we also translate the RRSP figure onto an after-tax estate basis, so you see both numbers.

- All assumptions are hypothetical. The interest rates, the 20-year horizon, the estimated 2026 Ontario tax brackets, and the fee estimates are illustrative — not quotes or guarantees. Tax brackets and benefit rates are indexed and change every year; figures are rounded.

- This is for general education only. Nothing here is personalized financial, tax, or legal advice. Before leveraging home equity or making large portfolio withdrawals, always consult a Certified Financial Planner (CFP), a Chartered Professional Accountant (CPA), or a licensed mortgage professional.

With that clear, let's meet our couple.

The Subject: Meet David and Susan

To keep things realistic and compliant with Canadian tax rules, let's follow an Ontario retiree couple, David and Susan, both 65 and both receiving OAS.

- Their current income: A combined $30,000 a year from CPP and OAS — $15,000 of taxable income each. At this income level, they also qualify for roughly $9,900 a year in Guaranteed Income Supplement (GIS), which is non-taxable and paid on top.

- Their home: Worth about $400,000, owned mortgage-free.

- Their goal: They need exactly $100,000 of extra cash in hand today for a roof repair and a home accessibility renovation.

- Their investment return: Their remaining RRSP funds earn a steady 6%, compounded annually.

These inputs stay fixed for every calculation that follows.

The Two Paths: Refinancing vs an RRSP Withdrawal

David and Susan face one core decision. Do they refinance — borrow against the home they already own — or do they withdraw from their RRSP?

Refinancing (home equity). Three ways to do it, and they behave very differently:

- A conventional cash-out refinance: a new mortgage registered on the home, with mandatory principal-and-interest payments and full bank qualification.

- A secured HELOC: a lower rate than most options, but mandatory monthly payments and strict qualification.

- A reverse mortgage: no mandatory payments ever, with the option to make voluntary interest-only payments.

- RRSP withdrawal. Pulling the cash directly from registered savings. It feels free because it is their own money, but without proper structuring, taxes and benefit clawbacks can quietly erode long-term wealth in the background.

- A standalone benchmark. For completeness, we also include an unsecured line of credit, which is not tied to the home at all.

The real question is not just where the cash comes from. It is which path protects the most wealth over the next 20 years, once every dollar is measured on the same scale.

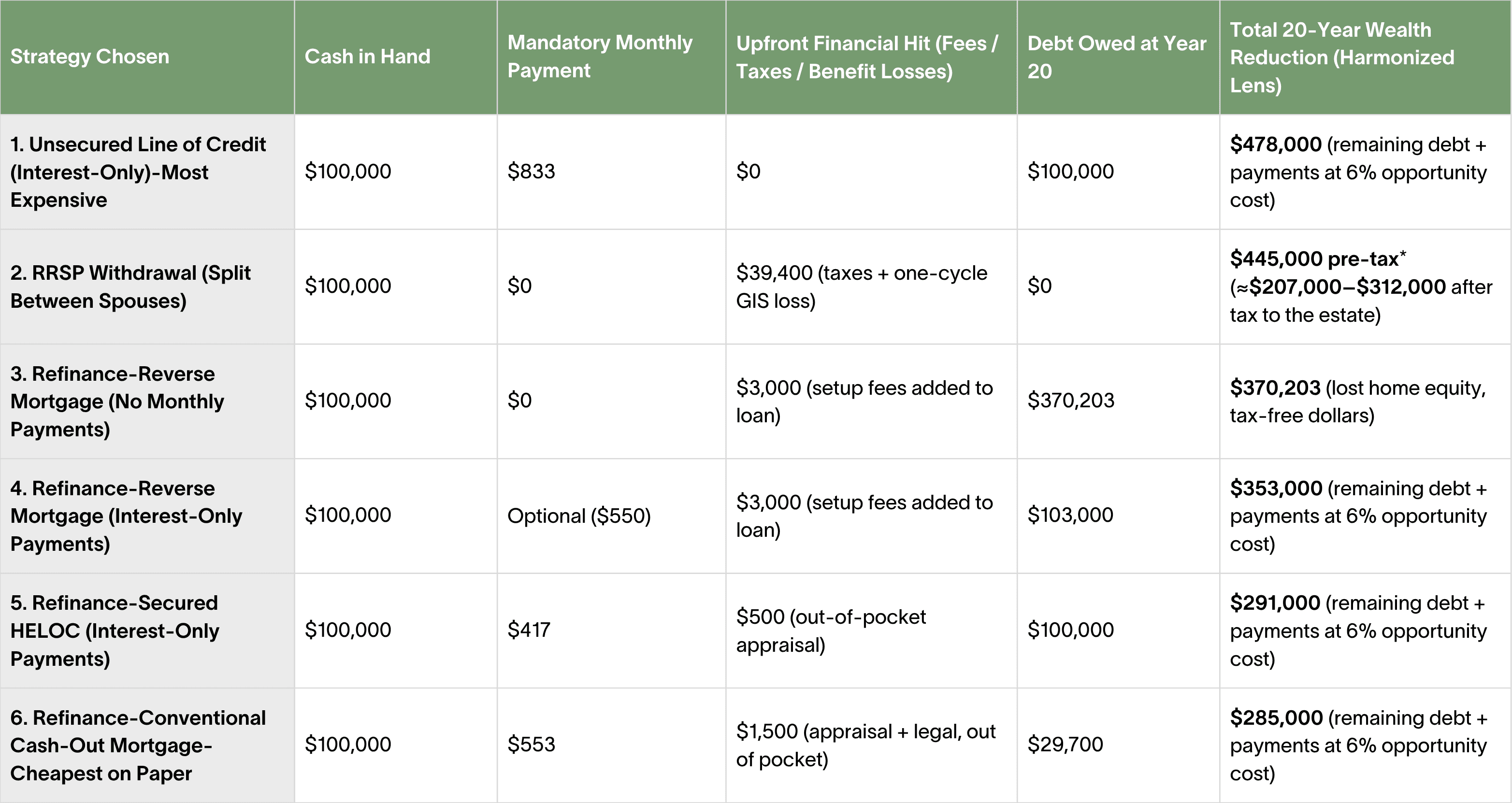

The Outcome: Ranked From Most Expensive to Cheapest

Once we harmonize the math by applying a 6% opportunity cost to every dollar spent or withdrawn over 20 years, here is how the six options stack up. Rankings are on a pre-tax harmonized basis — watch the asterisk on the RRSP row.

*The RRSP asterisk: the $445,000 is pre-tax registered money. Because those funds would eventually be taxed anyway — on withdrawal or on the second spouse's final return — their true after-tax value to the family is roughly $207,000 to $312,000. On that basis, the RRSP row drops from second-most-expensive to among the cheapest. The full explanation is in the deep dive below.

Note: the two cheapest options on paper — the HELOC and the conventional refinance — are the two this couple almost certainly cannot qualify for. These rankings hold true for this exact scenario only.

The Deep Dive: How the Math Actually Works

The Standalone Benchmark: Unsecured Line of Credit (The Most Expensive)

Many people assume an unsecured line of credit is safer because it never touches home equity. On a harmonized 20-year lens, it is actually the heaviest wealth destroyer of the group.

- The math: At an assumed 10% interest rate, David and Susan must pay $833.33 every single month just to keep the loan from compounding. Over 20 years, they pay $200,000 in nominal interest while still owing the original $100,000.

- The harmonized cost: Because that $833.33 is drained out of pocket instead of staying invested at 6%, the total 20-year opportunity cost plus principal climbs to roughly $478,000.

- The reality check: Qualifying for a $100,000 unsecured line on a $30,000 base income is virtually impossible under standard debt-service underwriting. And on this budget, those payments would realistically be funded by extra RRSP withdrawals — adding a tax cost the headline number doesn't even show. That hidden drag applies to every mandatory-payment option in this comparison.

The RRSP Lump-Sum Withdrawal (Competently Planned and Split)

Here is where careful planning changes everything. Because Canada taxes individuals rather than households, a poorly planned withdrawal — one spouse taking the entire amount — would trigger roughly $55,200 in immediate income tax plus a full clawback of that spouse's OAS, about $8,900 more. A competently planned strategy splits the income equally between David and Susan. If the savings sit in one name, converting to a RRIF and using the pension income-splitting election (available at 65+, up to 50% of the income) achieves the same result on paper — and RRIF withdrawals at 65+ also unlock the $2,000 pension income credit each, trimming the bill slightly further.

- Step 1 — The gross-up tax. To net exactly $100,000, they withdraw a combined gross total of about $129,500, roughly $64,750 each. The total tax bill across both returns is about $29,500. Standard withholding (around 30%) applies at source, with the exact figures trued up at tax filing.

- Step 2 — Protecting Old Age Security. Each spouse's individual income lands near $79,750 ($15,000 base plus $64,750 withdrawn) — safely below the 2026 individual OAS clawback threshold of $95,323. Their OAS stays completely untouched: $0 lost. A world apart from the one-name mistake above.

- Step 3 — The GIS cliff. GIS is calculated on combined household non-OAS income and runs on a July-to-June cycle based on the prior year's income. The withdrawal spike wipes out their roughly $9,900 GIS for one cycle. No planning can avoid this on a six-figure withdrawal.

- Step 4 — Replacing the GIS, almost for free. To cover that gap, they withdraw another ~$9,900 the following year — and here is the quiet lesson of this whole case study: at a $15,000 base income, that small top-up is essentially tax-free, fully sheltered by the basic personal and age credits. Small withdrawals at low income cost almost nothing; it is the concentrated spike that gets taxed. (Strictly, the top-up trims the next GIS cycle a little too — a fading ripple we cut off here.)

- Step 5 — The 20-year opportunity cost. Removing roughly $139,400 in total from a tax-sheltered portfolio compounding at 6% represents a future pre-tax asset value of about $445,000.

- The estate nuance: Registered money is pre-tax money. Whether it comes out gradually at modest rates or lands on the second spouse's final return at up to 53.5% in Ontario, the true after-tax value of that $445,000 to their heirs is roughly $207,000 to $312,000. Measured on that after-tax estate basis, the optimized withdrawal costs less than the $370,203 of tax-free home equity consumed by a no-payment reverse mortgage — across the entire range. That edge is real, but it rests on two things: the 6% return actually materializing, and the family caring about estate value rather than monthly cash flow. These are the real RRSP withdrawal tax consequences most people never model.

Refinancing Option A: The Conventional Cash-Out Refinance (The Literal "Refi")

This is the product the word "refinancing" technically means: registering a new mortgage on the home and taking the equity as cash.

- The math: At an assumed 4.5% five-year fixed rate with a 25-year amortization, borrowing $100,000 costs $553.47 per month in mandatory principal-and-interest payments, plus roughly $1,500 out of pocket for the appraisal and legal work.

- The harmonized cost: Because the payments steadily repay principal, only about $29,700 is still owing at year 20. Payments at 6% opportunity cost plus the remaining debt total roughly $285,000 — the cheapest option in the entire comparison.

- The reality check: It is also the least attainable. Banks must qualify borrowers at a stress-tested rate roughly two points above contract — pushing the qualifying payment to about $670 a month, or $8,000 a year of debt service on a $30,000 income. Add property taxes and heat, and the debt-ratio limits are blown past. And a five-year term over a 20-year plan means four renewals at unknown future rates.

Refinancing Option B: The Secured HELOC

- The math: At an assumed 5% rate with a $500 out-of-pocket appraisal, mandatory interest-only payments run $416.67 per month, and the $100,000 principal never shrinks.

- The harmonized cost: Payments at 6% opportunity cost plus the untouched principal produce a 20-year wealth reduction of about $291,000.

- The catch: Like the conventional refinance, a HELOC is mortgage-secured bank credit — so the federal stress test and strict income qualification apply. Proving the cash flow to service a $100,000 HELOC on a $30,000 base retirement income is exceptionally difficult. The second-cheapest option on paper is, again, one most fixed income retirees cannot actually get.

Refinancing Option C: The Reverse Mortgage

The third way to unlock home equity is built specifically for this situation: it qualifies on age and equity rather than income, and it never requires a payment. Two ways to structure it:

C1. With no monthly payments

- The math: Loan proceeds are completely tax-free, so taxable income stays at $30,000 — OAS and GIS are untouched today. Setup fees averaging $3,000 are added to the loan, making the starting balance $103,000. On their $400,000 home, that is about a 26% advance — comfortably inside the roughly 25–40% of home value that lenders typically offer 65-year-olds (the advertised 55% ceiling applies to much older borrowers).

- The 20-year cost: Canadian reverse mortgage interest compounds semi-annually. At an assumed 6.5% with no payments, the debt grows to $370,202.75, directly reducing the equity left in the home. A no-negative-equity guarantee means the family can never owe more than the home's fair value.

- The reality check: Most common reverse mortgage terms last 5 years, so a flat 6.5% for two decades assumes away renewal risk across as many as four renewals. And preserving the RRSP doesn't negate the taxes — it defers them: mandatory RRIF minimums begin the year after age 71, generating taxable income that erodes GIS in their later years anyway.

C2. With voluntary interest-only payments

- The math: From the $103,000 balance, the exact monthly interest is $550.51. Paying it keeps the principal flat: $132,121.97 paid over 20 years, $103,000 still owing.

- The harmonized cost: Through the 6% opportunity-cost lens, the total wealth reduction is about $353,000.

- The flexibility advantage: These payments are entirely optional. They can be paused without penalty during an emergency — breathing room no bank product offers.

The Key Takeaway

For David and Susan, there is no single winner that applies to everyone — and that is the real lesson. Measured on a fair, harmonized 20-year lens:

- An unsecured line of credit is the most expensive path and among the hardest to qualify for.

- A properly split RRSP withdrawal is dramatically better than the common one spouse mistake, and on an after-tax estate basis it beats a compounding reverse mortgage in this scenario.

- The conventional refinance and HELOC are the two cheapest options on paper — and the two a $30,000-income household cannot realistically obtain.

- The reverse mortgage is the one refinancing route that actually opens for this couple: it protects cash flow, shields OAS and GIS today, and offers unmatched payment flexibility. Its case rests on accessibility and cash flow, not on out-earning the loan.

How you refinance in retirement — and how you plan the tax side of any withdrawal — can be worth hundreds of thousands of dollars over time.

When the Rankings Could Change

This order is not universal. Watch for these factors:

- A different withdrawal size. Small annual withdrawals at this couple's income are nearly tax-free — but for GIS recipients, dripping money out exposes every year to the 50% GIS clawback, while one concentrated spike sacrifices a single cycle. Counterintuitively, for GIS households, one big planned hit often beats a slow drip.

- One-RRSP households. The split strategy needs either two RRSPs or the RRIF income-splitting election at 65+. Younger retirees or common-law situations without the election lose much of the tax advantage.

- No GIS in the picture. At higher base incomes, the GIS cliff disappears and the RRSP path gets cheaper still — until the OAS clawback zone appears near $95,000 per person.

- Interest rates and renewals. Every borrowing option here carries rate-reset risk over 20 years; a two-point move reorders the table.

- A shorter horizon or different return. Compounding — for and against you — is gentler over 10 years than 20, and the 6% assumption drives the RRSP math in both directions.

- Estate intentions. If leaving maximum value matters, the after-tax lens favours the planned withdrawal; if monthly cash flow and flexibility matter most, the reverse mortgage's case strengthens.

- Qualification ability. A retiree who can pass the stress test unlocks the cheaper bank options this couple cannot.

Who This Scenario Is Relevant For

This case study is most useful if you see yourself in David and Susan. It speaks directly to:

- Canadian homeowners aged 55+ who own their home or hold significant equity

- Retirees living mostly on CPP, OAS, and GIS with limited monthly cash flow

- Seniors who need a large one-time sum for renovations, medical costs, or family support

- Anyone weighing a refinance vs RRSP withdrawal decision

- Retirees worried about how a withdrawal might trigger an OAS clawback or GIS loss

If your income, equity, and goals look similar, the lessons here will likely apply — though your exact numbers will differ.

Your Next Step: Get Your Own Numbers Reviewed

Remember the disclosure at the top. This is one scenario with fixed assumptions. Your income, your goals, your property, and your timeline could reorder these results entirely. The smartest move is never to copy a generic example — it is to run your own exact numbers with people who work for you.

That is where two specialist teams come in:

- For your refinancing strategy, talk to us at Canadian Reverse Mortgage Advisors. We sit on your side of the table, compare every Canadian reverse mortgage lender, weigh them against your HELOC and refinance options, and model your real home equity choices side by side — so you can decide with confidence, at no cost to you.

- For your personalized tax picture, connect with our colleagues at Zen Tax. They can calculate your exact brackets, model a spousal withdrawal split or RRIF-splitting election, and confirm your OAS and GIS impact.

Together, these two perspectives give you the full picture — the borrowing side and the tax side — so nothing gets missed.

Refinancing vs RRSP Withdrawal FAQs

About the Author

Alexander Gasenko

Mortgage Broker, Reverse Mortgage Specialist

Alexander is the founder of Canadian Reverse Mortgage Advisors team and a licensed mortgage professional serving Ontario, British Columbia, and Alberta. With a degree in Economics and a background in banking, he’s passionate about helping Canadian seniors protect their equity and navigate rising living costs. When he’s not negotiating with lenders, Alexander shares financial insights on his YouTube channel, empowering Canadian homeowners to make informed decisions. His mission? To provide clarity and confidence for a secure financial future.