How to Identify Genuine Reverse Mortgage Products

If you’re considering a reverse mortgage, it’s important to understand both the benefits and the safeguards designed to protect homeowners. While reverse mortgages can boost your retirement income with no monthly payments, not every no-payment loan marketed to seniors is regulated or safe.

What is a Reverse Mortgage? A reverse mortgage allows Canadian homeowners aged 55+ to access tax-free funds from their home equity, without monthly payments, while remaining in their home. For a detailed breakdown, see our 2026 Reverse Mortgage Guide.

Some products may appear similar to regulated reverse mortgages because they allow interest to accumulate without monthly payments, but they lack the essential legal protections and home equity protection offered by true regulated reverse mortgages. Failing to spot the difference can leave retirees unprotected and at risk of unexpected debt or even the loss of their home.

The Red Flag Checklist: Is It a Regulated Reverse Mortgage?

The Financial Consumer Agency of Canada (FCAC) sets out strict criteria that define a true Canadian reverse mortgage. If an equity product does not meet these standards, it’s likely a private or alternative equity loan. While alternative loans can have a place in some situations, they do not offer the essential protections that retirees need. Watch for these key red flags:

🚩 Red Flag 1: No Age Requirement (55+)

A regulated reverse mortgage is only available to homeowners aged 55 and older. This age requirement protects you because lenders base the loan on your life expectancy, ensuring the solution is built to last. If a product has no age limit, it’s likely a short-term equity loan instead. Without the 55+ rule, the lender can’t guarantee a lifetime solution—meaning you may have to sell your home or refinance when the loan expires.

🚩 Red Flag 2: No "No Negative Equity" Guarantee

This guarantee is the most important protection for Canadian seniors. It ensures your final loan balance will never exceed your home's fair market value, providing a safe exit strategy for your estate, as long as you pay property taxes and insurance. Without this safeguard, a drop in the housing market could leave you or your heirs responsible for any shortfall. Without a "no negative equity" guarantee, borrowers face real financial risks if home values fall.

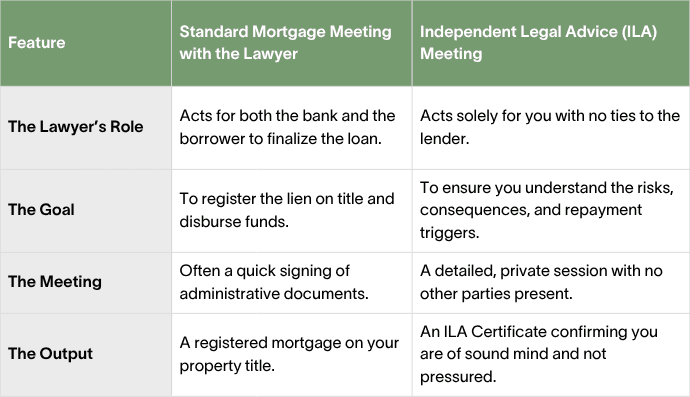

🚩 Red Flag 3: No Requirement for Independent Legal Advice (ILA)

To help protect your retirement, it’s essential to know the difference between a standard legal closing and Independent Legal Advice (ILA). Many homeowners think that simply meeting with a lawyer covers them fully. In reality, ILA is your main layer of safety with a regulated reverse mortgage. This requirement ensures you get advice from a lawyer working only for you, so you understand every part of the agreement before moving forward.

What is ILA, and How Does It Protect You?

Canadian regulations require a two-step legal process for reverse mortgages. This approach protects you from undue influence and ensures you clearly understand the long-term impact on your estate.

Table 1: Standard Mortgage Lawyer Meeting vs. an Independent Legal Advice

Prefer clarity and peace of mind? Learn more about us and see how our team guides Canadians in choosing the right regulated reverse mortgage products. Helping you make informed, confident decisions is our priority.

Regulated Reverse Mortgages vs. Other Interest-Accruing Products

Don’t confuse short-term, interest-accruing loans with regulated reverse mortgages. While both may skip monthly payments, only regulated reverse mortgages offer strong, long-term protections for seniors. These safeguards and guarantees designed to keep you and your home secure are unique to regulated products and should always be a priority for retirees.

- Regulated Reverse Mortgages: These provide a comprehensive long-term solution. You don't need an "end date" or an "exit strategy." You can remain in your home for as long as you choose with confidence.

- Private Interest-Accruing Loans: These offer temporary financial relief. Lenders design them for brief periods, requiring a clear plan to repay the loan or refinance later.

For Canadian seniors, knowing the difference between regulated reverse mortgages and other equity loans is essential. This understanding helps you make smarter, safer choices when unlocking your home’s value for retirement.

The Evolving Reverse Mortgage Market in Canada

The reverse mortgage market in Canada has grown rapidly in recent years. Canada’s largest lender, HomeEquity Bank, has originated over $1 billion in reverse mortgages annually for the past four years.

This surge reflects a growing demand among Canadians 55 and older for tax-efficient ways to unlock home equity and stay in their homes. More retirees now look to reverse mortgages as a flexible solution to support their financial goals in retirement.

As the reverse mortgage market expands and more lenders enter the Canadian space each year, it’s essential to know exactly what defines a regulated reverse mortgage.

Want to know which lenders offer regulated reverse mortgages in Canada? See our trusted lender list here.

Curious how much tax-free funds you could unlock? Try the Reverse Mortgage Calculator for a personalized estimate in under 30 seconds.

Not just another mortgage - real guidance for your financial peace of mind.

About the Author

Alexander Gasenko

Mortgage Broker, Reverse Mortgage Specialist

Alexander is the founder of Canadian Reverse Mortgage Advisors team and a licensed mortgage professional serving Ontario, British Columbia, and Alberta. With a degree in Economics and a background in banking, he’s passionate about helping Canadian seniors protect their equity and navigate rising living costs. When he’s not negotiating with lenders, Alexander shares financial insights on his YouTube channel, empowering Canadian homeowners to make informed decisions. His mission? To provide clarity and confidence for a secure financial future.